relevancia

estadística y predictiva. Las variables que incrementan la confianza en un

banco están relacionadas con una mayor tasa de alfabetización financiera,

mejores estrategias de diversificación del riesgo, mayores ingresos per cápita

por hogar, así como la proximidad a los bancos. La edad y el acceso a internet

también son variables importantes para dichas evaluaciones. El modelo CatBoost presenta un valor AUC robusto para la recuperación

de la precisión de 0.734. El estudio propuesto contribuye a dos objetivos

principales diferentes: (i) la aplicación de una combinación de modelos

econométricos con algoritmos modernos de aprendizaje automático.

Keywords:

confianza en los bancos; inclusión financiera; aprendizaje automático; métodos

de encuesta; México.

JEL: G21;

D14; O16; C55; C25

Introduction

This research examines the

determinants of trust in banks (TIB) in Mexico using individual‐level data from the National Survey of Financial

Inclusion (ENIF)’s 2021 and 2024 waves. This study’s major research question

is: "What predicts TIB among Mexican adults?" When depositors trust

that banks will safeguard their deposits and honor commitments, the cost of

transactions is low and the markets of credit and savings are more efficient (Knack & Zak, 2003). From a socio‐psychological perspective, trust itself denotes

voluntary vulnerability based on positive beliefs about a counterparty’s

ability and kindness (Hu et al., 2019). Applied to the context of banking, this refers to

depositor confidence regarding intermediaries to behave responsibly and

truthfully, thereby encouraging participation in formal financial services (Ahmad et al., 2021).

In addition to individual

characteristics, our empirical framework includes state-level infrastructure

measures (ATMs, branches, TPOS-equipped establishments) and INEGI’s Safety

perception index as higher-level controls. To compare

machine learning classifiers to standard estimates of the logistic regression

model. While our analysis will take into consideration state-specific

infrastructure measures, the direct relationship between micro-trust metrics

and national aggregates is a topic for future research. ENIF 2021-2024 offers

micro-data for the six regions in Mexico. In consideration of the disparate

confidence level that the public may have toward the financial system, our

analysis will focus on the variation of Trust in Banking (TIB) for individual

conditions. Persistent distrust is a barrier; this study identifies which

attributes and contexts predict trust to safeguard deposits and honor

obligations.

The aim of this study is twofold. First, it aims to

determine which individual, and contextual factors have the largest bearing on TIB

among Mexican adults. Second, it endeavors to estimate the contribution of

banking infrastructure and digital service provision to confidence using

machine-learning algorithms (Chen & Guestrin, 2016) for prediction and logistic regression for

inferential work.

We hypothesized here that greater financial capability—more financial knowledge and more disciplined

money-management practices—would be accompanied by greater TIB. We also posited

that access to the internet and smartphones (digital inclusion) and usage of

internet/mobile banking, along with denser local financial infrastructure

(branches, ATMs, and point-of-sale terminals), would each positively correlate

with TIB. We predicted a positive correlation of perceived neighborhood

security with TIB and lower TIB in less safe local conditions. For

demographics, we predicted a positive effect of education and income to

increase TIB and a nonlinear (inverted-U) effect of age. We finally predicted

risk attitudes consistent with contemporary portfolio theory—understanding the

risk–return trade-off and support of diversification—to forecast TIB and

investigated whether the mean TIB is different from 2021 to 2024 levels

conditioning upon covariates.

Consistent with these expectations, our empirical

analysis reveals that infrastructural and digital‐access variables are the strongest predictors of

depositor confidence. In logistic regression, a one‐unit increase in digital‐access (smartphone ownership and household internet

availability) raises the probability of trusting banks (TIB = 1) by approximately

8 percentage points (pp) (p < .001), with branch-network availability

showing a positive marginal effect on TIB, whereas normalized ATM density

exhibits a statistically significant negative marginal effect. These results

highlight the usefulness of combining machine learning with classical

econometric approach to analyze emerging markets.

These findings highlight the usefulness of combining nonlinear machine learning

with classical methods to analyze trust in emerging markets. 2. Literature

Review Trust in financial institutions is essential to financial inclusion and

the efficient functioning of banking systems.

This work, through the inclusion of granular

constructs for trust and national infrastructure metrics, has a number of contributions to make to literature and policy.

This work advances theories about institutional forms of trust that show how

physical and virtual banking infrastructure complement each other and encourage

deposits and applies machine learning for accuracy and conformity with policy

relevance.

Literature Review

Trust in financial institutions is essential

to financial inclusion and the efficient functioning of banking systems. A

broad international literature point that higher levels of institutional trust

are positively associated with bank account ownership, the use of formal

financial services, and overall financial stability (Fungáčová et al., 2019). In emerging economies with

greater informality and uncertain institutions, trust is crucial for

individuals' participation in the formal financial sector.

From an institutional perspective, past

research emphasize regulation, banking supervision,

and deposit‐insurance

schemes as mechanisms that reduce uncertainty and promote systemic trust (Knell & Stix, 2015). However, further studies indicate that the perceived

credibility on these warrants among depositors are

just as important as their effectiveness (Butzbach, 2016). Therefore, poor enforcement, limited transparency,

or low awareness of consumer protections may undermine trust even in the

presence of formal safeguards.

More over, evidence from empirical research suggests that trust in banks

is a multidimensional construct shaped by economic,

social, and psychological factors. Mayer, Davis, and Schoorman

(Mayer et al., 2006) propose a framework to understand

organizational trust, which comprehends three key dimensions: ability,

benevolence, and integrity. This framework has been widely applied to financial

institutions. A research by Cruijsen,

de Haan, and Roerink

(van der Cruijsen et al., 2021), employing European survey data, shows that higher

levels of financial knowledge are associated with greater trust in banks and

financial authorities. In contrast, negative personal experiences with

financial institutions tend to wear away trust in a persistent manner.

Recent studies have highlighted the

growing relevance of digital financial inclusion to physical banking

infrastructure in influencing levels of trust in financial institutions. For

example, banking trust could be boosted by improved digital safety as well as

improved service quality and handling of client data (Bijlsma et al., 2022). On the other hand, adoption in technology cannot

guarantee improved trust if concerns in these two areas still linger (Koomson et al., 2023). Similarly, physical bank branches often function as

“symbols of trust,” although their marginal importance may decline as digital

channels expand (Sakong & Zentefis, 2024).

Contextual conditions, especially

perceived public security, is another factor that plays a significant role in

shaping institutional trust. In the Mexican context, Blanco (2013), who analyzed the impact of insecurity and crime

victimization on support and satisfaction in institutions, shows that lower

trust in public and financial institutions are

associated with higher levels of crime and insecurity. This finding concurs

with comparative evidence suggesting that local insecurity operates as an

indirect channel through which confidence in banks and other formal

institutions is weakened (Broekhoff et al., 2024).

Scholarship in methodology views

machine learning as a way to improve empirical

economics by increasing the precision of prediction and simplifying complex

problems, thus complementing other methods instead of displacing them,

especially in policy studies ((Mullainathan & Spiess, 2017). Nonetheless, the literature overlooks the strength

of hybrids that combine machine learning methods with causal inference.

More recent studies have used

machine learning algorithms for analyzing trust in banks, proposing that trust

in banks cannot be fully explained using econometric analysis, due to possible

nonlinearities or interaction patterns (Adamyk et al., 2019). Based on World Values Survey data, using an

integrated approach combining both econometric tools and machine learning

algorithms, Adamyk et al. (2019) analyzed how

different factors interact to influence trust in banks. The study confirms that

individual properties and global trust have proved to play an important role in

forming trust in banks. Forecasting approaches will provide enhanced

effectiveness if they are theoretically informed and integrated with techniques

for improved clarity.

However

critical these advances have been, the literature that applies them to Mexico

is very limited, especially in the area of nationally

representative surveys using machine learning tools and theories of trust. The

National Financial Inclusion Surveys carried out in Mexico in 2021 and 2024

present a unique opportunity to close the gap, since these surveys include

comprehensive information on financial behavior, feelings of security,

availability of financial infrastructure, and opinions. The goal of the current

research work is to perform a comprehensive study on the determinants of trust

in banks using the aforementioned tools, with direct

policy implications regarding financial inclusion in Mexico.

Empirical

evidence on determinants of trust in banks

Prior studies link higher financial knowledge to

greater trust in banks, with similar patterns for broader financial

institutions—supporting the view that knowledge and disciplined money

management raise TIB (van der Cruijsen et al., 2021). Digital

access and use tend to complement trust when security and reliability are

credible; during COVID-19, trust in banks’ payment services rose alongside

digital payments, but mere uptake without security/UX improvements does not

necessarily increase trust (Jafri et al., 2024). Physical presence also matters:

branches act as “symbols of trust,” and branch/ATM density is associated with

inclusion and service confidence (Sakong & Zentefis, 2024). In Mexico and the region, perceived insecurity

depresses institutional trust, implying higher TIB where neighborhood security

is stronger(Blanco, 2013).

Trust generally increases with income and follows

mixed, life-cycle patterns by education and age; attitudes aligned with the

risk–return trade-off and diversification correlate with higher confidence in

financial services (Fungáčová & Weill, 2019;

Jafri et al., 2024). Historically, a sizable share of unbanked adults in Mexico

cited lack of trust as a barrier, while recent waves emphasize income/need;

accordingly, we model TIB jointly with digital inclusion, financial

infrastructure, and perceived security to capture the main channels through

which confidence is formed.

Theoretical Framework

Trust

in banking rests on a firm belief that institutions will safeguard assets,

honor commitments, and act with integrity (Mayer et al., 2006). This belief is shaped by three core dimensions—

technical competence, benevolence toward depositors, and adherence to ethical

norms—which together determine depositor confidence in both individual banks

and the broader financial system (Butzbach, 2016).

Formal

structures such as regulation, deposit insurance, and supervisory oversight

provide

“Structural

assurances” that reduce uncertainty and reinforce institutional trust (Zucker, 1986). At the same time, sociological perspectives remind us of that trust functions as a shortcut under uncertainty,

relying on reputational signals and probabilistic judgments in the absence of

complete information (Luhmann, 2018).

Within

Mexico’s financial landscape, depositor trust emerges from judgments about a

bank’s solvency and fairness, filtered through cultural norms and moral beliefs

(Alraheb et al., 2019). Confidence is forged both through formal

channels—such as CNBV oversight and IPAB insurance—and informal influences like

branch reputation and community word‐of‐mouth,

reflecting the coexistence of traditional banking, rural microfinance, and

digital platforms.

Analyzing financial behavior requires understanding

the interplay between personalized trust, developed through repeated

interactions, and systemic trust, based on market protection and stability.

Pooled cross-sectional ENIF data (2021 and 2024) offers insights into the

factors influencing bank choices.

Methodology

Data Sources and Sample

We use the 2021 and

2024 waves of Mexico’s ENIF, conducted by CONAIF and collected by INEGI. ENIF

is a nationally representative household survey covering financial behaviors,

perceptions, and access/infrastructure in urban and rural areas. A stratified,

multistage cluster design ensures national and regional representativeness;

across both waves 30,548 households were surveyed (15,291 in 2021; 15,257 in

2024), with oversampling of small localities (<2,500 inhabitants). Response

rates were 91% (2021) and 90.5% (2024). After standard cleaning (listwise

deletion and removal of incomplete records), the final analytic sample is

27,056 adults—13,554 (2021) and 13,502 (2024). Both waves had INEGI Ethics

Committee approval, complied with Mexico’s data-protection law, obtained

informed consent, and were released in anonymized form.

Variable Construction

Dependent Variable: Trust in Banks (TIB)

Following Sztompka’s (Sztompka, 1999) “Reflected

Trustworthiness” framework, we operationalize TIB as a composite of five binary

indicators embedded in Section 11 of ENIF (“Confianza

y protección”) (INEGI, 2022). Respondents

answered “Sí” (Salazar-Cruz

& Román-Reyes) (1) or “No” (2) to

each of the following statements:

1. P11_1_1. “Si tuviera

que solicitar servicios de un banco… ¿considera que recibiría toda la

información necesaria?” (Trust that the bank will

provide complete information)

2. P11_1_2. “…

¿considera que resolverían su necesidad o problema económico?” (Trust that the bank will

resolve its economic needs/problems)

3. P11_1_3. “…

¿considera que estaría seguro su dinero?” (Trust that the bank will

keep funds safe)

4. P11_1_4. “…

¿considera que resolverían sus quejas y reclamaciones?” (Trust that the bank will

handle complaints)

5.

P11_1_5. “… ¿considera que protegerían sus datos personales?” (Trust that the bank will protect personal

data)

Each

item (P11_1_1 – P11_1_5) was recoded as a binary indicator (1 = “Sí”; 0 = “No”; missing if “No sabe/No contestó”).

A summative index (TRUST_SUM) was constructed as the sum of these five dummies,

yielding a discrete scale ranging from zero (no trust in any dimension) to five

(full trust on all five dimensions). For models requiring a continuous input,

we also compute a normalized average (TIB = TRUST_SUM / 5), which ranges from 0

to 1.

The

TIB index draws on items that directly map onto the trust dimensions proposed

by Mayer et al. (2006): two items capture

ability (e.g., technical competence of banks and perceived security of

deposits), two assess benevolence (e.g., banks’ concern for customer welfare

and fairness in fee practices), and one reflects integrity (e.g., transparency

in communication and adherence to ethical standards).

Key Predictors

Financial

knowledge, behavior, and attitudes (measurement framework)

We

measure financial capability in components to preserve construct validity and

2021–2024 comparability. Knowledge is an ENIF 5-item index (interest/inflation)

common to both waves—not the Lusardi–Mitchell “Big Three,” which requires a

diversification-knowledge item absent in ENIF(Lusardi & Mitchell, 2011). Behavior is

captured by a Financial Accountability Index (budgeting/record-keeping) aligned

with OECD-INFE (Atkinson &

Messy, 2012). Attitudes

(risk–return recognition; preference for diversification) enter as separate

controls; we therefore do not form a 2024-only OECD composite.

Financial

knowledge (ENIF 5-item). We construct a

financial knowledge index from five factual items on interest and inflation

available in ENIF-2021 and ENIF-2024 (INEGI, 2022; 2025). This ENIF-based

measure is not the Lusardi & Mitchell “Big Three,” which includes a

diversification-knowledge item that ENIF does not provide consistently across

waves (Lusardi & Mitchell, 2011). Four items originate from Section 12

(interest calculations and inflation adjustment), and one item originates from

Section 4.7 (inflation definition). Each indicator is coded as 1 if the

respondent’s answer is correct, and 0 otherwise, as follows:

1.

Inflation Definition (P4_7_1) (INEGI, 2022): Respondents

evaluate whether “Inflation means that the price of things increases”. A

correct response (code 1, “True”) was coded as fknowledge_inflation

= 1; any other response (codes 2, 8, 9) was coded as 0.

2.

Simple Interest (P13_1) (INEGI, 2022), (P12_1) (INEGI, 2025): Respondents answer

the question, “If you lend 25 pesos to a friend and the next week they

return the 25 pesos, how much did you pay in interest?” The correct answer

(“Nothing,” code 1) was coded as fknowledge_interest_simple

= 1; any other response (codes 2–4, 9x) was coded as 0.

3.

Annual Interest(P13_2) (INEGI, 2022), (P12_2) (INEGI, 2025): Respondents

evaluate “Let's suppose that you deposit 100 pesos in a savings account that

gives 2% a year, without deposits or withdrawals, how much will you have at the

end of the year?” The correct answer (“102 pesos,” code 2) was coded as fknowledge_interest_annual = 1; all other codes were coded

as 0.

4.

Compound Interest (P13_3) (INEGI, 2022), (P12_3) (INEGI, 2025): Respondents

evaluate “If you deposit 100 pesos reinvesting the interest, what will you

have at the end of five years?” The correct answer (“110 pesos,” code 2,

since 100 × (1.02)^5 ≈ 110.41) is coded as fknowledge_compound = 1; all other codes are coded as 0.

5.

Inflation‑Adjusted Value

(P13_4) (INEGI, 2022), (P12_4) (INEGI, 2025): Respondents

evaluate “If you are given 1,000 pesos but you have to wait a year with

inflation of 5%, could you buy the same?” The correct answer (“No,” code 2)

was coded as fknowledge_inflation_corrected = 1; all

other responses (codes 1, 3, 4, 9x) were coded as 0.

Subsequently, these five binary variables are

summed to create a composite financial knowledge score (fknowledge_score),

such that fknowledge_score ∈ {0, 1, 2, 3, 4, 5}:

This raw score was then normalized to a

continuous index (Financial Knowledge Index) bounded

between zero and one, defined as:

![]()

Higher values of Financial

Knowledge Index correspond to greater overall financial‑knowledge proficiency.

Financial

accountability index. Coded as Financial Accountability Index we operationalize financial accountability as a composite measure of

six core budget- and expense-tracking behaviors, all drawn from ENIF (INEGI,

2022, 2025) survey items P4_1 and P4_2 sub-questions. For each

respondent i, we define the binary indicators

as follows:

1. budg_recordᵢ = 1 if respondent “maintains a written record of

income and expenses” (P4_1=1);

2. exp_noteᵢ = 1 if they “annotate expenses” (P4_2_1=1);

3. sep_fundsᵢ = 1 if they “separate payment funds from daily

spending” (P4_2_2=1);

4. rec_notesᵢ = 1 if they “track receipts/debts to avoid missed

payments” (P4_2_3=1);

5. mgmt_appᵢ = 1 if they “use an app or tool for expense tracking”

(P4_2_4=1);

6. autopayᵢ = 1 if they “have automatic (domiciled) bill

payments” (P4_2_5=1).

These six indicators are summed to yield a financial accountability score,

and ranges from 0 (no behaviors) to 6 (all behaviors).

We then normalized this value to a 0–1 index.

![]()

This index captures the extent to which each

respondent actively monitors and manages their personal finances. In OECD-INFE

terminology, this index corresponds to the behavior pillar and is modeled

separately from knowledge and attitudes (Atkinson & Messy, 2012).

Risks. Attitudes

(risk perceptions). In line with Lusardi & Mitchell (2011) and OECD-INFE

guidance, risk perceptions are treated as attitudes, not knowledge. We

therefore include two attitudinal indicators from ENIF (INEGI, 2022; 2025):

·

First, Risk_opportunity captures awareness of the trade‐off

between easy gains and losses. Specifically, Risk_opportunity is set to 1 if the respondent

affirms the statement “If someone offers you the chance to win money easily,

you can easily lose it too” (P4_7_2 = 1), and 0 otherwise.

·

Second, a variable labeled Risk_diversify

captures belief in diversification by coding as one respondent who agrees with “It's

better to save money in two or more ways or places than just one” (P4_7_3 =

1), and 0 otherwise.

In

subsequent analyses, both Risk_opportunity and

Risk_diversify enter as distinct predictors: the

former gauges sensitivity to potential losses associated with high‐return opportunities, whereas the latter

reflects a preference for spreading financial resources across multiple saving

channels. These attitudinal variables are not included in the Financial

Knowledge Index; under the OECD-INFE view they belong to the attitudes pillar,

and under the LM view they are distinct from factual knowledge.

Demographic and

Socioeconomic Controls

•

Age and Age Squared: (Allen et al.,

2016) (INEGI, 2025) Respondent’s age in

years (Courbage &

Nicolas, 2021); age_sq

= AGE² to capture nonlinear age effects.

•

Sex: (SEXO) (INEGI, 2022, 2025) Sex (0 = female;

1 = male).

·

Educational

attainment (NIV) (INEGI, 2022, 2025): was grouped into five levels: none,

elementary, middle school, high school, and higher education. For the

survey-weighted logistic regression, schooling enters as four dummies

(elementary, middle, high, higher), with no schooling as the omitted reference;

marginal effects are interpreted relative to this base. For machine-learning

models (Random Forest, XGBoost, LightGBM,

CatBoost), the same categories are encoded via

one-hot vectors to avoid imposing ordinality and to capture nonlinearities and

interactions. Responses of “don’t know/unstated” are set to missing. This

approach aligns the regression tables and ML features and replaces the

incorrect min–max “Scholar_norm” description.

·

Marital Status: (P3_2) (INEGI, 2022, 2025). Three dummies: MARRIED, where "Vive

con su pareja en unión libre" (“lives with their partner in a

common-law union) and "Está casada(o)"

(married) status were considered jointly;

SINGLE, for "Es soltera(o)"; and,

UNPARTNERED, for which "Está separada(o)"

(apart) , "Está divorciada(o)"

(divorced), and "Es viuda(o)"

(widow/widower) were considered in this category.

·

Labor‐Force Participation

(LFP) (P3_5) (INEGI, 2022, 2025): LFP = 1 if currently employed, self‐employed or searching for job; 0 if out of the

labor force such as students, retired or housewife.

·

Monthly Household Income (thousand Pesos):

Monthly household income was constructed from two ENIF items: the reported

earnings amount (P3_11A) and frequency of payment (P3_11B) (INEGI, 2022, 2025). Specifically, P3_11A records the respondent’s gross

earnings in pesos (ranging from 00000 = “No recibe ingresos” to 90000, with 98000 = “98 000 y más” and 99888 = “No responde”).

P3_11B indicates the payment interval (1 = semanal, 2

= quincenal, 3 = mensual, 4

= anual). To convert all observations into a common

monthly metric, the following algorithm was applied:

•

Observations coded P3_11A = 00000 (“no income”)

or P3_11A = 99888 (“no responde” no response) were

set to zero. The resulting income_monthly variable

(in pesos) was then rescaled to thousands of pesos (income_m_thous

= income_monthly / 1 000) to improve

interpretability. For inclusion in the machine-learning models, income_m_thous was normalized to the [0, 1] interval using

min‐max scaling:

![]()

This procedure ensured the comparability of

monthly income across all respondents, regardless of their original pay

frequency.

Behavioral/Infrastructural

Control

·

Cash usage index. This index is constructed from

two ENIF (INEGI, 2022, 2025) survey items: one for small purchases

(P7_1_1) and one for large purchases (P7_1_2).

For minor purchases,

the use of cash is coded 3, also for major purchases. For each good, a binary

indicator is formed, where 1 denotes the use of cash and 0 denotes the non-use.

Finally, the two

binary indicators are averaged to construct the Cash_usage_index,

ranging from 0 to 1. A value of 1 indicates using cash on big and small

purchases, while 0 indicates no cash usage. Intermediate values represent

partial use of cash. The index averages values from both responses and is used

in regression and machine-learning models to predict bank trust.

·

Digital access.

The digital access

variable measures respondents' accessibility to digital services, such as

owning a smartphone (P3_14) (INEGI, 2022, 2025), where a response of ‘yes’ is coded as 1 and ‘no’ is coded as 0. It also includes

Internet access in the household (P0_4_2) (INEGI, 2022, 2025), with ‘yes’ coded as 1 and ‘no’ coded as 0. The results are then

averaged from both responses and used to predict trust in banks through

regression and machine-learning models.

Financial-Infrastructure

and Regional Variables

We

include four state-level variables drawn from INEGI (INEGI, 2025)

banking-establishment and public-security databases:

State-Level Banking

Infrastructure:

·

ATM_number_norm is the number of

ATMs in respondent’s region (INEGI, 2022, 2025), normalized between [0,1].

·

Bank_branches_norm is the number of

bank branches in the respondent’s region (INEGI, 2022, 2025), normalized

between [0,1].

·

Estab_TPOS_norm is the number of establishments

with point-of-sale terminals in the respondent’s region (INEGI, 2022, 2025),

normalized between [0,1].

·

Security perception. Designated as the Safety_perception_index, this

variable assesses the population's perception of security within the

corresponding region. The data is from

the Encuesta Nacional de Victimización y

Percepción sobre Seguridad Pública (ENVIPE) (INEGI, 2021). Is an indicator of the percentage of Mexicans who feel

secure in their municipality, neighborhood, or house. This indicator is

constructed from INEGI's (2021, 2023) national household surveys

and represents insecurity perception and not a crime rate. The Regional

Security Perception Index was weighted by each state’s population for this

study. Subsequently, the Safety Perception Index was normalized using the

min-max method to obtain values ranging between 0 and 1.

Each respondent was assigned a value for these four

variables corresponding to their state of residence. In all regression and ML

models, these counts (and the index) are entered as continuous covariates,

capturing how regional banking infrastructure and security conditions shape

individual trust in banks.

Regional and Locality

Controls:

·

Locality size. Refers to the

population size of the respondent’s locality as identified by ENIF (INEGI,

2022, 2025). The categories were: 1 = 100,000 inhabitants or more; 2 = 15,000

to 99,999 inhabitants; 3 = 2,500 to 14,999 inhabitants; 4 = less than 2,500

inhabitants. This variable was coded as Locality_size_norm,

where the values are between 0 and 1, from normalization to the categories.

·

Region:

ENIF (INEGI, 2022, 2025) is divided into six geographic regions: 1 = Northwest,

2 = Northeast, 3 = Occident-Bajio, 4 = Mexico City, 5 = South Central-Orient; 6 = South.

These regions were coded as one-hot using dummy variables.

·

Year:

This is a binary variable that indicates the ENIF year, where 0 represents 2021

and 1 represents 2024.

Empirical

Strategy

The

empirical approach comprises two complementary techniques: (1)

logistic-regression models to estimate the marginal effects and statistical

significance of predictors on a binary trust outcome; and (2) tree-based machine-learning

(ML) algorithms, to capture nonlinearities and interactions while assessing

relative feature importance.

Dependent Variable Specification

Because the principal research question is

“Which factors predict TIB among Mexican adults?” we define a binary target as:

![]()

Logistic-Regression Model

We begin with a baseline logistic-regression

specification:

where:

·

Education was a dummy variable for elementary, middle

school, high school and higher. Edu_none (no education)

is omitted from the analysis.

·

Civil Status are dummy variables for Married_partnered and Unpartnered. Single

is omitted.

·

LFP is a dummy variable where 1 is a participant

and 0 is a non-participant.

·

Regions are dummies for regions 1–5 (Region 6 =

South is omitted).

Coefficients are

reported as average marginal effects (dy/dx) in the

sample means (Williams, 2012).

Multicollinearity

diagnostics

We evaluated for

multicollinearity by using variance inflation factors (VIF). The mean VIF was

2.64, with a small subset of expected temporospatial controls (year and

regional infrastructure variables) exhibiting higher values, all remaining

below conservative thresholds. (Salmerón et al.,

2020). In fact, these are manifestations of

expected temporospatial relationships, not a problem of linear dependence.

Thus, it is apparent that multicollinearity is not a problem that affects

stability and interpretation of coefficients. Also, multicollinearity is

largely a problem of parametric inference, and tree machine learning models

used in this analysis do not suffer from multicollinearity.

Machine-learning Models

This

study employs four tree-based machine-learning classifiers to model individual

trust in banks. In addition, a stacking ensemble is implemented as a

complementary approach to assess whether combining base learners improves

predictive performance. All features were provided to the machine-learning

pipeline as a pre-encoded matrix: categorical predictors were converted to

their numeric representations in advance, and continuous variables were normalized

with values between [0, 1]. Automated validation procedures systematically evaluate data for

out-of-range values, target imbalances, and feature-integrity concerns, thereby

ensuring high data quality prior to modeling.

Predictive

modeling leverages a sophisticated ensemble architecture comprising four

complementary base learners:

•

Random Forest for robust bagging (Mullainathan

& Spiess, 2017)

•

XGBoost for regularized

gradient boosting (Chen &

Guestrin, 2016)

•

LightGBM for

high-performance, leaf-wise boosting (Ke et al., 2017)

•

CatBoost for seamless

categorical handling (Prokhorenkova et

al., 2018)

Base‐model predictions are fused via a stacking

ensemble: a LightGBM meta-learner integrates the out-of-fold

predictions from each base learner. Stratified 5-fold cross-validation (Berrar, 2019) guides both

hyperparameter tuning and performance estimation, whereas sigmoid and isotonic

calibration refine the reliability of the predicted probabilities.

The

hyperparameter optimization is fully automated. An initial RandomizedSearchCV

phase quickly explores broad parameter ranges, after which Optuna

conducts multi-objective tuning while simultaneously optimizing the accuracy,

F1-score, and ROC-AUC. Memory‐management routines

dynamically monitor RAM usage and downcast data types where possible, thereby enabling

efficient training on large survey datasets.

Model

evaluation is comprehensive, encompassing:

•

Classification metrics (accuracy, precision,

recall, F1-score)

•

Ranking metrics (ROC-AUC, average precision)

•

Calibration metrics (log loss, reliability

diagrams)

This

is, model performance is evaluated using complementary metrics, including the

area under the receiver operating characteristic curve (ROC–AUC) and the

precision–recall area under the curve (PR–AUC). While ROC–AUC summarizes the

model’s ability to discriminate between outcomes across classification

thresholds, PR–AUC places greater emphasis on correct classification of the

positive class, which is particularly informative in settings with class

imbalance.

In

addition to individual classifiers, a stacking approach is employed. Stacking

is an ensemble-learning technique that combines the predictions of multiple

base models to generate a final prediction, potentially improving performance

by exploiting the strengths of different algorithms. All machine-learning

models used in this study are tree-based, meaning they rely on recursive

partitioning of the data and are well suited to capturing nonlinear

relationships and interaction effects.

Optimal

decision thresholds are identified via Youden’s J statistic, and a suite of

visual diagnostics—ROC and precision-recall curves, feature‐importance bar plots, and correlation

heatmaps—facilitates transparent comparison across models.

To

elucidate the drivers of banking trust, the pipeline integrates

interpretable-ML techniques. SHAP (Lundberg &

Lee, 2017) provides local and

global explanations using TreeExplainer, LinearExplainer, and KernelExplainer,

generating interactive force, dependence, and summary plots. Permutation‐importance analyses and model‐specific feature rankings were further

accompanied by statistical significance testing to confirm the robustness of the

identified predictors.

Statistical

validity was ensured by the following:

•

Variance Inflation Factor analyses to detect

multicollinearity

•

Parametric coefficient estimation for

interpretable effect sizes

•

Confidence intervals around predicted

probabilities

•

Model diagnostics, including residual analysis

and goodness-of-fit tests

Inference and robustness

considerations

Statistical inference, including

standard errors and confidence intervals, is conducted within the logistic

regression framework, where coefficient estimation and hypothesis testing are

well defined. In contrast, the primary objective of the machine-learning models

is predictive performance rather than parameter inference. Accordingly,

robustness in the machine-learning context is assessed through out-of-sample

validation and performance stability across alternative algorithms and metrics.

Specifically, model performance is evaluated using

cross-validation procedures and complementary metrics such as ROC–AUC and

precision–recall AUC. Consistent results across models provide evidence of

robustness to model specification and sample variation. This combined approach

allows the analysis to benefit from formal statistical inference in the

econometric model while exploiting the flexibility of machine-learning methods

to capture nonlinearities and heterogeneous effects.

Results

Logistic Regression Results

Survey‐weighted logistic regression was used to

identify the individual-level determinants of TIB = 1). The estimation sample

included 27,056 respondents (design degrees of freedom = 2,171), representing a

population per year as shown in Table 1, of:

Table 1

Population representation

ENIF 2021, 2024

|

Year |

Population |

|

2021 |

90,328,320 |

|

2024 |

94,221,441 |

|

Total |

184,549,761 |

Source: Authors’ elaboration with data from INEGI (2021, 2025)

The

overall model was highly significant (F (27, 2145) = 41.92, p < .001).

Tables 2 and 3 present the full coefficient estimates and average marginal

effects, respectively.

The analysis of marginal effects (dy/dx) revealed several salient factors that influence

individuals’ trust in banks. Notably, the squared term for age demonstrated

that as respondents’ ages increased to higher extremes, the probability of

reporting trust in banks decreased substantially -25.8 pp. Educational

attainment emerged as a significant predictor, with completion of secondary

education associated with a +7.4 pp, and higher education yielding a comparable

effect +7.2 pp, relative to those without formal education.

Household income, measured as a one-unit

increase in normalized income, was robustly associated with greater trust in

banks (+58.8 pp). Financial knowledge (+19.4 pp) and financial accountability (+13.3

pp) were also strong positive determinants. In terms of access to financial

services, greater digital accessibility corresponded to a 7.5 pp increase in

trust, whereas higher dependence on cash (-4.5 pp) and residency in smaller

urban localities (-3.5 pp) were associated with lower trust levels.

Table 2

Logistic regression coefficients

|

TIB |

Coefficient |

Std. Err. |

P>t |

|

Sex |

0.0153181 |

0.0432281 |

0.723 |

|

Age_sqr |

-1.1799730*** |

0.1372356 |

0.000 |

|

Elementary |

-0.0664667 |

0.0610764 |

0.277 |

|

Middle school |

0.1385063 |

0.0730802 |

0.058 |

|

Highschool |

0.3381847*** |

0.068433 |

0.000 |

|

Higher |

0.3308259*** |

0.0749043 |

0.000 |

|

Married_partnered |

-0.1403426** |

0.0518044 |

0.007 |

|

Unpartnered |

-0.0900615 |

0.0685769 |

0.189 |

|

LFP |

-0.1083240* |

0.051841 |

0.037 |

|

Income_norm |

2.6875290*** |

0.4314828 |

0.000 |

|

Financial_knowledge_index |

0.8873147*** |

0.1529521 |

0.000 |

|

Financial_accountability_index |

0.6079980*** |

0.0823243 |

0.000 |

|

Risk_opportunity |

0.1739683*** |

0.0442976 |

0.000 |

|

Risk_diversify |

0.2363627*** |

0.0446844 |

0.000 |

|

Digital_access |

0.3434786*** |

0.0697817 |

0.000 |

|

Cash_usage_index |

-0.2045666** |

0.0761589 |

0.007 |

|

Locality_size_norm |

-0.1578039** |

0.0600514 |

0.009 |

|

Bank_branches_norm |

2.4021510* |

1.15286 |

0.037 |

|

ATM_number_norm |

-5.4898470* |

2.630328 |

0.037 |

|

Estab_TPOS_norm |

3.9191910* |

1.789483 |

0.029 |

|

Safety_perception_index |

2.6854610*** |

0.7285679 |

0.000 |

|

Region_Northwest |

1.2151530** |

0.3884239 |

0.002 |

|

Region_Northeast |

2.5338500* |

0.9912105 |

0.011 |

|

Region_Occident_Bajio |

-1.1799070* |

0.4874668 |

0.016 |

|

Region_Mexico_City |

2.1992760** |

0.6555795 |

0.001 |

|

Region_CentralSouth_Orient |

-0.3814723* |

0.1557763 |

0.014 |

|

Year |

0.1022517 |

0.1949696 |

0.600 |

|

_cons |

-2.8954170*** |

0.8024116 |

0.000 |

Survey-weighted average marginal effects; robust

standard errors clustered at PSU; weights = FAC_PER; strata = EST_DIS; PSU =

UPM_DIS

*** p<.001, ** p<.01, * p<.05

Source: Own calculations based on INEGI (2020–2025)

Table 3

Marginal effects

|

dy/dx |

std. err. |

P>t |

|

|

Sex |

0.0033531 |

0.0094619 |

0.723 |

|

Age_sqr |

-0.2582902*** |

0.0298098 |

0.000 |

|

Elementary |

-0.0145492 |

0.0133679 |

0.277 |

|

Middle school |

0.0303183 |

0.0159884 |

0.058 |

|

Highschool |

0.0740269*** |

0.0148813 |

0.000 |

|

Higher |

0.0724161*** |

0.0163479 |

0.000 |

|

Married_partnered |

-0.0307203** |

0.0113132 |

0.007 |

|

Unpartnered |

-0.019714 |

0.0150006 |

0.189 |

|

LFP |

-0.0237116* |

0.0113534 |

0.037 |

|

Income_norm |

0.5882865*** |

0.0940043 |

0.000 |

|

Financial_knowledge_index |

0.1942287*** |

0.0333362 |

0.000 |

|

Financial_accountability_index |

0.1330877*** |

0.0178853 |

0.000 |

|

Risk_opportunity |

0.0380808*** |

0.0096809 |

0.000 |

|

Risk_diversify |

0.0517386*** |

0.009731 |

0.000 |

|

Digital_access |

0.0751857*** |

0.0152294 |

0.000 |

|

Cash_usage_index |

-0.0447786** |

0.016667 |

0.007 |

|

Locality_size_norm |

-0.0345425** |

0.0131446 |

0.009 |

|

Bank_branches_norm |

0.5258187* |

0.2522871 |

0.037 |

|

ATM_number_norm |

-1.2017000* |

0.5756083 |

0.037 |

|

Estab_TPOS_norm |

0.8578912* |

0.3916022 |

0.029 |

|

Safety_perception_index |

0.5878338*** |

0.1593508 |

0.000 |

|

Region_Northwest |

0.2659908** |

0.0849523 |

0.002 |

|

Region_Northeast |

0.5546470* |

0.2168825 |

0.011 |

|

Region_Occident_Bajio |

-0.2582758* |

0.106701 |

0.016 |

|

Region_Mexico_City |

0.4814105** |

0.1433888 |

0.001 |

|

Region_CentralSouth_Orient |

-0.0835024* |

0.0341324 |

0.015 |

|

Year |

0.0223824 |

0.0426762 |

0.600 |

Survey-weighted average marginal effects; robust

standard errors clustered at PSU; weights = FAC_PER; strata = EST_DIS; PSU =

UPM_DIS

*** p<.001, ** p<.01, * p<.05

Source: Authors’ own calculations based on INEGI

(2020–2025)

Regarding institutional

infrastructure, a one-unit increase in the density of bank branches was

positively related to trust (+52.6 pp), whereas a similar increase in ATM

availability exhibited a negative association (-120.2 pp). The presence of

point-of-sale (POS) terminals was also positively associated with trust in

banks (+85.8 pp).

Perceptions of safety within the

banking environment also contributed substantially; a one-unit increase in

perceived safety resulted in a +58.8 pp increase in trust. Attitudinal factors,

such as risk tolerance measured by opportunity-seeking (+3.8 pp) and

diversification preferences (+5.2 pp), were both significantly positively

correlated.

With respect to sociodemographic

characteristics, being married (-3.1 pp) and participation in the labor force (-2.4

pp) were marginally associated with reduced trust. Regional heterogeneity was

evident: compared to the reference region, respondents in the Northeast (+55.5

pp) and Mexico City (+48.1 pp) exhibited greater trust in banks, whereas those

in the Occident‐Bajio

(-25.8 pp) and Central‐South‐Orient (-8.4 pp) regions reported lower levels of

trust.

The goodness‐of‐fit

test for the survey‐weighted

logistic model yielded the following:

F (9, 2163) = 2.26, p = 0.0164.

Under the null hypothesis, the

model is correctly specified, and its predicted probabilities do not

systematically differ from the observed outcomes. We reject this null

hypothesis because p<0.05, indicating that there remains a statistically

significant lack of fit even after accounting for our 27 predictors and survey

design. Therefore, it is necessary to utilize machine-learning models, which

are designed to capture complex nonlinearities and interactions, as a

complementary approach to uncover patterns that the logistic model may not

detect.

Machine‐Learning Results

Because TIB = 1 constitutes the majority class in our

hold-out sample (16 338/27 056 ≈ 60.39 %), the baseline precision in a

Precision–Recall framework is 0.6039,

not “near zero.” In other words, a naïve classifier that randomly labels

observations as “trust” with the same frequency as in the data would achieve an

average precision of 0.6039. Therefore, we assessed our models’ lift over the baseline when reporting the PR-AUC (Saito & Rehmsmeier, 2015).

Table 4 reports the performance of the four

machine-learning classifiers and the stacking ensemble, benchmarked against a

random baseline. A baseline precision of 0.6039 reflects at 60.39 % prevalence

of TIB = 1 in the hold-out set, indicating that a random classifier would

correctly flag trusting respondents only at that rate. Among the algorithms, CatBoost attained the highest PR-AUC (0.7339) and the

strongest ROC-AUC (0.6634), along with low log-loss (0.6503) and narrowly

outperforming RandomForest (PR-AUC = 0.7317; ROC-AUC = 0.6617; log-loss =

0.6526). However, RandomForest was ultimately preferred owing to its superior

probability calibration and lower variance in log-loss across cross-validation

folds. XGBoost and LightGBM

delivered nearly identical discrimination (PR-AUC ≃ 0.731; ROC-AUC ≃ 0.662), underscoring the robustness of tree-based

ensembles, whereas the stacking ensemble underperformed (PR-AUC = 0.7233;

ROC-AUC = 0.6492), suggesting limited incremental benefit from combining these

models.

Table 4

Classifier results comparison: four base

learners and one stacking ensemble

|

Model / Baseline |

PR-AUC |

ROC-AUC |

Log-loss |

Opt. Threshold |

Accuracy |

Precision |

Recall |

F₁ |

|

Baseline

(random) |

0.6039 |

– |

– |

– |

– |

– |

– |

– |

|

RandomForest |

0.7317 |

0.6617 |

0.6526 |

0.5262 |

0.6114 |

0.7226 |

0.5786 |

0.6427 |

|

XGBoost |

0.7315 |

0.6613 |

0.6473 |

– |

0.6216 |

0.7111 |

0.6288 |

0.6674 |

|

LightGBM |

0.7309 |

0.6614 |

0.6427 |

0.5151 |

0.6353 |

0.7001 |

0.6928 |

0.6964 |

|

CatBoost (best

single model) |

0.7339 |

0.6634 |

0.6503 |

0.4942 |

0.6310 |

0.7056 |

0.6674 |

0.6860 |

|

Stacking

Ensemble |

0.7233 |

0.6492 |

0.6371 |

0.6199 |

0.6035 |

0.7049 |

0.5906 |

0.6427 |

Source: Authors’ calculations using ENIF 2021 (INEGI, 2022) and ENIF 2024 (INEGI, 2025)

Feature importance

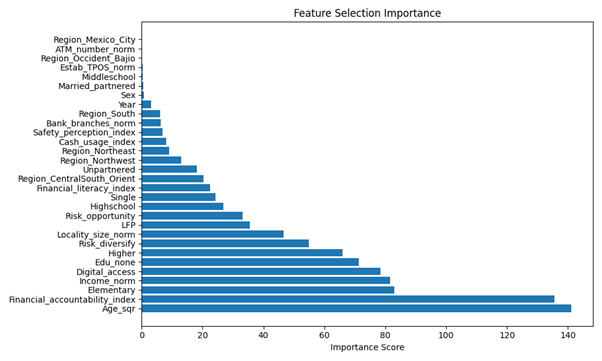

The feature-importance chart

(Figure 1) ranks each predictor by how much it reduces impurity (or “gain”)

across all trees in the best single model.

To investigate the determinants

of model performance, several key patterns emerge from the feature importance

analysis. The most important predictor is the squared age variable (Age_sqr), which has an importance

value of almost 140. This result shows the strong nonlinear relation of age to

trust: Trust levels are maximized in mid-adult life, with a sharp decrease when

age is either low or high.

Figure 1

Feature selection importance

Source: Authors’ elaboration using data from INEGI (INEGI, 2020)

Financial Accountability Index

reaches an importance measure of over 130. This

underscores the primary value of individuals’

perceived financial capability and reports an attitudinal measure second only

to age in terms of predictive power. Socioeconomic status and access to major

resources variables formed the subsequent level of predictive variables, whose

importance measures usually resided in the 70–90 interval. This list consisted

of education attainment (eminently so at ‘none’ and at the elementary level),

normalized household income (Income_norm), and access

to computers (digital access). Higher education is another feature of this

area. Overall, these results indicate the primary role education, income, and digital

access play in discriminating between those who reported trusting and those who

did not.

A second group of predictors,

with mid-level importance values between 40 and 65, consists of attitudinal and

contextual factors like risk preferences (Risk_diversify

and Risk_opportunity), locality size (Locality_size_norm), participation in the labor force

(LFP), and the Financial Knowledge Index. These factors have a significant

impact on trust predicted, although their relative

strength is moderate when we consider the stronger socioeconomic drivers. Finally, demographic and infrastructural variables, such

as sex, marital status, regional indicators, ATM density, and POS‐terminal density had the lowest importance scores

(below 30). These findings suggest that, once the principal attitudinal and

structural factors are accounted for, such demographic and infrastructural

characteristics contribute only marginal predictive value to the model.

Overall, the ranking confirms

that demographic nonlinearity (Courbage & Nicolas, 2021) and financial attitudes (accountability and

knowledge) are the engines of the model, while basic socioeconomic status and

digital access further sharpen its discrimination, and purely geographic or

infrastructural measures play only a minor role.

Synthesis and Comparison

Both approaches converge on the

centrality of socioeconomic status and financial attitudes for TIB: household

income, financial accountability, and digital access consistently rank among

the top predictors in the logistic and ML models. They also agree that

risk-diversification attitudes and digital engagement are positively associated

with trust. Where they differ is informative: ML surfaces a pronounced nonlinear

age profile—captured by the squared term (Age_sqr)—with

trust peaking in mid-adulthood and tapering at younger and older ages; the

logistic model flags Age_sqr as significant but less

richly. ML further elevates the role of basic educational attainment,

suggesting interactions and multi-path mechanisms that parametric models may

understate. By contrast, regional indicators are significant in the logistic

regressions but fall in ML importance rankings, likely because tree-based

ensembles absorb spatial heterogeneity through finer individual-level features.

Taken together, the methods are complementary. Both

identify shared foundations—financial capability and access—while ML adds value

by revealing nonlinearities and interactions that standard specifications

obscure. The emerging narrative is that trust in banks is anchored in material

and perceptual access to financial resources, yet the pathways that build trust

are multidimensional and context-sensitive.

Discussion

Key Findings

This study employs

both survey‐weighted logistic

regression and tree‐based machine‐learning (ML) models to identify the key

determinants of TIB among Mexican adults.

Both approaches converged on the centrality of socioeconomic status and

financial‐attitudinal

factors—household income, financial accountability, and digital access emerged

as the top predictors of depositor confidence.

The enhanced ML pipeline further uncovered a pronounced nonlinear age

effect: trust peaked in mid-adulthood and declined at both younger and older

extremes. Educational attainment, especially

the distinction between no formal education and elementary level, also

exhibited heightened importance in ML models, suggesting multidimensional

pathways linking basic schooling to trust that are not fully captured by

parametric methods.

Geographic

dummies, while significant in the logistic framework, played only a minor role

in the ML ranking, implying that ensemble methods internalize spatial

heterogeneity through more granular individual predictors. Finally, attitudinal measures of risk

diversification and engagement with digital financial services positively

contribute to trust, underscoring the interplay between risk orientation and

fintech adoption.

At the algorithmic

level, CatBoost attained the highest discrimination

(PR-AUC = 0.7339; ROC-AUC = 0.6634) before calibration and narrowly outperformed

RandomForest. However, Random Forest’s

superior probability calibration and lower log-loss variance recommended it for

policy‐relevant

applications. The feature‐importance analysis of the best single model

highlighted Age_sqr (≈ 140) and the Financial

Accountability Index (≈ 130) as the dominant drivers of predictive performance,

followed by education, normalized income, and digital access (importance scores

of 70–90). Mid-range factors (scores

~40–65) included perceived neighborhood security, risk attitudes, locality

size, labor-force participation, and financial knowledge, while purely

demographic or infrastructural variables (sex, marital status, regional

indicators, ATM/POS density) contributed marginally.

Comparison with Prior Literature

These

findings corroborate theoretical accounts that emphasize the joint role of

structural assurances (e.g., deposit insurance and regulatory quality) and

individual capabilities (financial knowledge and accountability) in fostering

institutional trust (Mayer, Davis, & Schoorman, 2006;

Zucker, 1986). The nonlinear age pattern we uncover is consistent with

life-cycle effects on financial behavior (Courbage

& Nicolas, 2021). The pronounced role of digital access accords with

evidence that improvements in digital payments can elevate trust in banks’

services (Bijlsma

et al., 2022) and with systematic

reviews highlighting trust and security as central to FinTech adoption (Jafri

et al., 2024). At the same time, the literature cautions that mere uptake

without credible security and usability gains may not raise trust—an

observation aligned with our result that digital access matters most when

paired with favorable security perceptions (del

Carmen Díaz-Peña et al., 2025).

Our comparatively

smaller effects for ATM/POS density relative to

digital access are compatible with work showing that branches often function as

“symbols of trust,” whose marginal salience can diminish as digital channels expand and service reliability is signaled through other

means (Sakong & Zentefis, 2024). The positive

income gradient and the mixed, life-cycle-shaped patterns for education and age

fall within the ranges documented in cross-country analyses of trust in banks

and in recent European evidence on trust in payment services (Fungáčová

et al., 2019). Finally, the

positive association between perceived neighborhood security and TIB echoes

Mexico-specific findings that crime and insecurity depress institutional trust (Blanco,

2013). Our findings show that in Mexico, digital

access, safety perceptions, and visible infrastructure together influence trust

in banks.

Limitations

There are several

caveats that warrant consideration.

First, the survey‐weighted logistic

model exhibited a statistically significant lack of fit (F(9,2163)=2.26, p=0.0164), implying that complex nonlinearities

remain unmodeled by parametric approaches.

Second, the cross-sectional design of the ENIF waves limits causal

inference and may be subject to reporting bias.

Third, national‐level financial

indicators (e.g., deposit/GDP) were not directly linked in the individual‐level analysis; future work could integrate

macro‐micro models to

strengthen external validity.

Conclusion

This study illustrates that TIB of Mexican adults has

a confluence of socioeconomic status, financial-behavioral practices, and

digital experiences. Household income and financial responsibility emerge as

among the very best predictors of TIB in survey-weighted logistic regression

and machine-learning models, and the nonlinear life-cycle pattern—reaching its

maximum at mid-life and declining at young and oldest ages—emerges most clearly

for tree-based learners. Lower levels of education

appear more significant within non-parametric analyses, which aligns with the

notion that schooling may influence trust through multiple channels.

Furthermore, digital access indicators and diversification attitudes

demonstrate that both secure engagement with fintech and prudent financial

behavior play central roles in supporting trust. From a methodological

perspective, ensemble learning algorithms such as CatBoost

and Random Forest demonstrate superior discriminatory ability (PR-AUC ≈ 0.73)

and enhance diagnostic feature analysis. These findings suggest that machine

learning approaches can effectively complement and extend traditional

econometric inference methods.

They imply three

practical levers for regulators and institutions: establish stronger

financial-capability programs—with emphasis on accountability practices and

core education—so confidence grows at scale; install safe and equitable digital

infrastructure and digital literacy, with tailored assistance for young and old

adults with particular barriers to online banking; and transmit service

reliability and consumer protections so that trust cues are salient. These

types of initiatives can augment personal confidence and, as a side effect,

support further macro objectives such as increasing

the bank-deposit/GDP ratio and sustaining inclusive growth. Because the design

is cross-sectional, causal inference is limited. A natural next step is

panel-based machine-learning with macro/financial shocks to trace trust

trajectories over time (Knell & Stix, 2015; Butzbach, 2016), interpret

model-based importances/SHAP patterns with formal theories of trust for sharper

mechanisms (Sztompka, 1999), and apply natural experiments—like deposit-insurance

reforms—to estimate impacts of policies. Including explicit macro–micro

linkages between aggregate financial indicators and trusting individuals would

further improve external validity. In combination, predictive analytics and

evaluation driven by theory offer practical guidance for bolstering trust and

inclusion in Mexico’s banking system.

Bibliographic References

Adamyk, B., Skirka, A., Snihur, K., & Adamyk, O.

(2019). Analysis of Trust in Ukrainian banks based on machine learning

algorithms.

Ahmad,

S., Hussain, F. Z., Naheed, K., & Shahid, M. S. (2021). An Empirical

Investigation of E-banking Service Quality Customer Trust and Customer Loyalty

of Pakistani Banks. Sustainable Business

and Society in Emerging Economies, 3(3),

319-326.

Allen,

F., Demirguc-Kunt, A., Klapper, L., & Martinez

Peria, M. S. (2016). The foundations of financial inclusion: Understanding

ownership and use of formal accounts. Journal

of Financial Intermediation, 27,

1-30. https://doi.org/https://doi.org/10.1016/j.jfi.2015.12.003

Alraheb, T.

H., Nicolas, C., & Tarazi, A. (2019). Institutional environment and bank capital ratios. Journal of Financial Stability, 43, 1-24.

Atkinson,

A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the

OECD/International Network on Financial Education (INFE) pilot study.

Berrar, D. (2019). Cross-validation. In M. Rehm & S.

König-Ries (Eds.), Encyclopedia of

Bioinformatics and Computational Biology (pp. 542-545). Elsevier.

Bijlsma,

M., van der Cruijsen, C., & Koldijk, J. (2022).

Determinants of trust in banks’ payment services during COVID: An exploration

using daily data. De Economist, 170(2), 231-256.

Blanco,

L. R. (2013). The impact of crime on trust in institutions in Mexico. European Journal of Political Economy, 32, 38-55.

Broekhoff,

M.-C., van der Cruijsen, C., & de Haan, J. (2024). Towards financial

inclusion: Trust in banks payment services among groups at risk. Economic Analysis and Policy, 82, 104-123. https://doi.org/10.1016/j.eap.2024.02.038

Butzbach,

O. (2016). Trust in banks: a tentative conceptual framework. Journal of Contextual Economics–Schmollers Jahrbuch(3), 303-330.

Chen,

T., & Guestrin, C. (2016). XGBoost:

A scalable tree boosting system. Proceedings of the 22nd ACM SIGKDD

International Conference on Knowledge Discovery and Data Mining, New York, NY.

Courbage, C., & Nicolas, C. (2021). Trust in insurance:

The importance of experiences. Journal

of risk and insurance, 88(2),

263-291.

del

Carmen Díaz-Peña, L., Sosa, F. A. P., Robles, R. D., & Sauza, R. M.

(2025). The Service-Dominant Logic as driver of financial inclusion in digital

payments sector: The case of E-fectivo. Revista Mexicana de Economía y Finanzas

Nueva Época REMEF, 20(4).

Fungáčová, Z., Hasan, I.,

& Weill, L. (2019). Trust

in banks. Journal of Economic Behavior

& Organization, 157,

452-476. https://doi.org/10.1016/j.jebo.2017.08.014

Hu,

Z., Ding, S., Li, S., Chen, L., & Yang, S. (2019). Adoption

intention of fintech services for bank users: An empirical examination

with an extended technology acceptance model. Symmetry, 11(3), 340.

INEGI. (2020). Census of Population and Housing 2020

(Censo de Población y Vivienda 2020) (

INEGI. (2021). Encuesta Nacional de Victimización y

Percepción sobre Seguridad Pública (ENVIPE) 2021 (

INEGI. (2022). Encuesta Nacional de Inclusión Financiera

(ENIF) 2021: Metodología.

INEGI. (2025). Encuesta Nacional de Inclusión Financiera

(ENIF) 2024: Metodología y resultados.

Jafri,

J. A., Amin, S. I. M., Rahman, A. A., & Nor, S. M. (2024). A systematic

literature review of the role of trust and security on Fintech adoption in

banking. Heliyon, 10(1).

Ke,

G., Meng, Q., Finley, T., Wang, T., Chen, W., Ma, W.,…Liu,

T.-Y. (2017). Lightgbm: A highly efficient gradient

boosting decision tree. Advances in

neural information processing systems,

30.

Knack,

S., & Zak, P. J. (2003). Building trust: public policy, interpersonal

trust, and economic development. Supreme

court economic review, 10,

91-107.

Knell,

M., & Stix, H. (2015). Trust in banks during normal and crisis

times—evidence from survey data. Economica, 82, 995-1020.

Koomson,

I., Koomson, P., & Abdul-Mumuni, A. (2023). Trust in banks, financial

inclusion and the mediating role of borrower discouragement. International Review of Economics &

Finance, 88, 1418-1431. https://doi.org/10.1016/j.iref.2023.07.090

Luhmann,

N. (2018). Trust and power. John

Wiley & Sons.

Lundberg,

S. M., & Lee, S. I. (2017). A unified approach to interpreting model

predictions. Advances in Neural Information Processing Systems 30, Long Beach,

CA.

Lusardi,

A., & Mitchell, O. S. (2011). Financial literacy and retirement planning

in the United States. Journal of pension

economics & finance, 10(4),

509-525.

Mayer,

R. C., Davis, J. H., & Schoorman, F. D. (2006).

An Integrative Model of Organizational Trust. In Organizational Trust (pp. 82-108): Oxford University PressOxford.

Mullainathan,

S., & Spiess, J. (2017). Machine learning: an applied econometric

approach. Journal of economic

perspectives, 31(2), 87-106.

Prokhorenkova, L., Gusev, G., Vorobev, A., Dorogush,

A. V., & Gulin, A. (2018). CatBoost: unbiased

boosting with categorical features. Advances

in neural information processing systems, 31.

Saito,

T., & Rehmsmeier, M. (2015). The

precision-recall plot is more informative than the ROC plot when evaluating

binary classifiers on imbalanced datasets. PloS one, 10(3), e0118432.

Sakong,

J., & Zentefis, A. (2024). Bank branch access:

Evidence from geolocation data. Olin

Business School Center for Finance & Accounting Research Paper(2023/12).

Salazar-Cruz,

L. M., & Román-Reyes, P. (2015). Continuities and changes in labor

participation in the State of Mexico during 2000-2012 period [Article]. Papeles de Poblacion, 21(83), 135-188.

Salmerón, R., García, C., & García, J. (2020). Overcoming

the inconsistences of the variance inflation factor: A redefined VIF and a

test to detect statistical troubling multicollinearity. arXiv preprint arXiv:2005.02245.

Sztompka, P. (1999). Trust:

A sociological theory. Cambridge University

Press.

van der

Cruijsen, C., de Haan, J., & Roerink,

R. (2021). Financial knowledge

and trust in financial institutions. Journal

of Consumer Affairs, 55(2),

680-714.

Williams,

R. (2012). Using the margins command to estimate and interpret adjusted

predictions and marginal effects. The

Stata Journal, 12(2), 308-331.

Zucker,

L. G. (1986). Production of trust: Institutional sources of economic

structure, 1840–1920. Research in organizational

behavior.